According to Sea-Intelligence, the evolution of capacity market shares among the three carrier alliances on the Transpacific and Asia-Europe routes has changed since the COVID-19 pandemic.

This analysis comes from Sea-Intelligence’s 640 issue of its weekly analytical report, Sunday Spotlight.

Capacity market share refers to the percentage of total deployed capacity in each trade lane operated by each of the three carrier alliances.

According to Sea-Intelligence, the alliances jointly lost capacity market shares on the Asia-North America West Coast, particularly during the pandemic, when capacity outside of the alliance frameworks was significantly deployed.

READ: Decline in US-Asia imports challenges global container recovery

Ocean Alliance regained its share in 2023, however the 2M alliance did not and is now positioned lower than it was prior to the pandemic.

Sea-Intelligence noted that 2M lost much of its pre-pandemic gain on the Asia-North America East Coast, while both Ocean Alliance and THE Alliance similarly lost capacity market share compared to the same pre-pandemic period.

Sea-Intelligence observed that THE Alliance acquired some market share during the pandemic, and with the loss of Ocean Alliance, the two alliances are effectively tied for second place behind 2M.

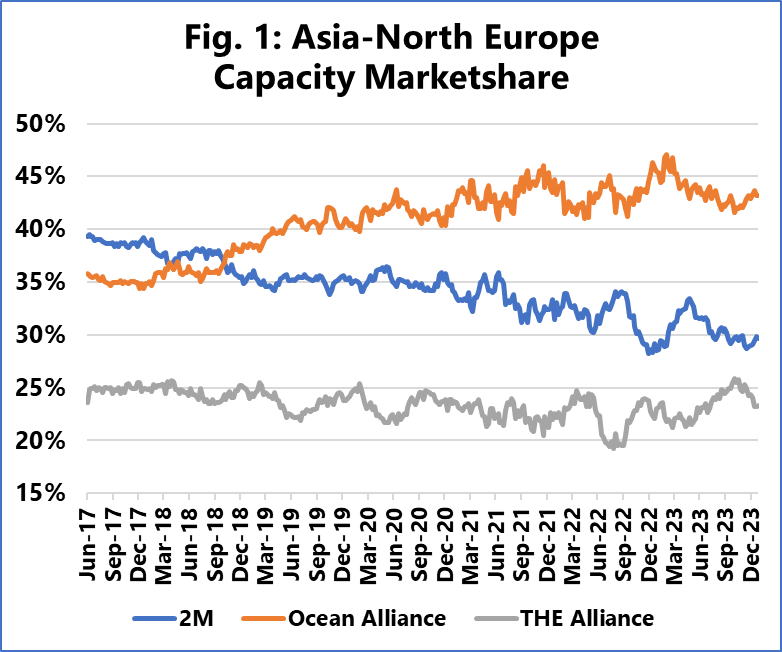

The significant change, however, is seen on Asia-North Europe (as shown in Figure 1).

READ: Pacific small box carrier share normalised

Alan Murphy, CEO of Sea-Intelligence, said: “THE Alliance has maintained a relatively stable presence on the trade lane, across the entire analysed period. 2M however, has seen a constant erosion, which has been taken over by Ocean Alliance.

“This is a development taking place over essentially the entire period and is therefore not linked to the beginning dissolution of 2M. Essentially, CMA CGM, COSCO and Evergreen, have clearly gained position into North Europe, at the relative expense of Maersk and MSC.”